A clear and accessible guide to how coverage works in America, who it is built for, and why the payment model behind the card matters as much as the card itself

By: Farzin Espahani

People often talk about health insurance in the United States as if it were one system. It is not. It is a collection of programs, private plans, public subsidies, age-based eligibility rules, and payment structures that developed over many decades. Some coverage is sponsored by the government. Some is sold by private insurance companies. Some is built mainly for people under age 65. Some is built for older adults and certain people with disabilities. Then beneath all of that is another question that matters just as much as the insurance card itself: how doctors, hospitals, and other providers are paid. That is where the difference between fee for service and value based care comes in.

That overlap is what makes the American system feel confusing. A person can have Medicare, but get it through a private Medicare Advantage plan. A person can have employer insurance, while the doctors in that network are being paid under a value based contract. A child can be covered through a public program, while the family buys separate dental coverage through a private insurer. Once you separate the system into a few basic questions, the structure becomes much easier to follow. Who sponsors the coverage? Which age group is it mainly built for? And how is care paid for behind the scenes?

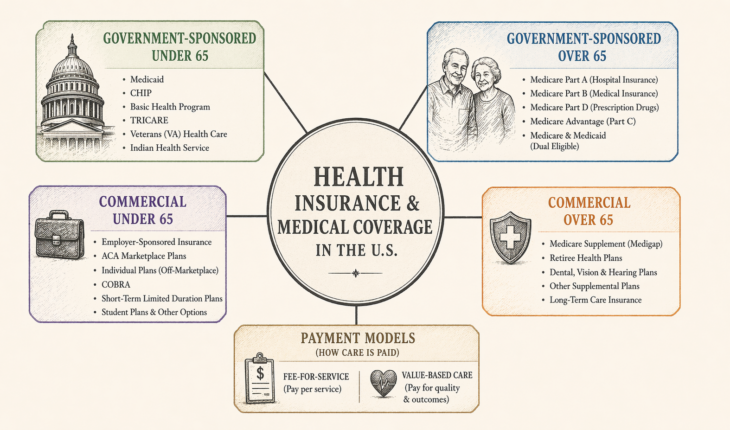

The cleanest way to map the U.S. system is in four boxes: government-sponsored coverage for people under 65, government-sponsored coverage for people over 65, commercial coverage for people under 65, and commercial coverage for people over 65. After that, it helps to explain fee for service and value based care, because those are payment models rather than insurance products in the usual sense.

Government-sponsored coverage for people under 65

For Americans under 65, the largest government-sponsored coverage program is Medicaid. Medicaid is funded jointly by the federal government and the states, and it covers many low-income adults, children, pregnant women, older adults with limited means, and people with disabilities. Because states have flexibility in how they run their programs, Medicaid feels somewhat different across the country, but the basic purpose is the same: to provide medical coverage to people who would otherwise struggle to get or keep it.

Closely related to Medicaid is the Children’s Health Insurance Program (CHIP). CHIP covers children in families with incomes too high to qualify for Medicaid but too low to comfortably afford private coverage. That middle ground matters in real life, because many working families earn too much for one program but still not enough to make commercial premiums and out of pocket costs feel manageable. CHIP exists to keep children from falling into that gap.

Some states also use the Basic Health Program. This is a state option allowed under federal law for certain low-income residents whose income may move above and below Medicaid and CHIP thresholds. Medicaid.gov describes the program as a way to provide more affordable coverage and improve continuity of care for people whose income fluctuates. That may sound technical, but the practical point is simple. In the United States, people often move in and out of eligibility because income changes. The Basic Health Program is one attempt to reduce that churn.

There are also public coverage systems that do not fit neatly into the usual Medicaid and Marketplace discussion. TRICARE covers many active duty service members, retirees, and military families. The Department of Veterans Affairs operates health care for eligible veterans. The Indian Health Service is the federal health program for American Indians and Alaska Natives who meet its eligibility rules. These programs matter because they show that government-sponsored medical coverage in the United States is broader and more varied than many people assume.

Government-sponsored coverage for people over 65

For most people over 65, the center of the system is Medicare. Medicare is a federal health insurance program that generally covers people age 65 and older, along with some younger people with disabilities or certain medical conditions. Medicare.gov explains the structure through several parts: Part A covers hospital insurance, Part B covers medical insurance such as physician and outpatient services, Part D covers prescription drugs, and Part C, better known as Medicare Advantage, is another way to receive Medicare-covered benefits through a private plan approved by Medicare.

Original Medicare usually means Part A and Part B together. It covers a large share of medically necessary care, but it does not mean every bill disappears. People still face deductibles, coinsurance, and other out of pocket exposure unless they have additional protection layered on top. That is an important point, because many people think turning 65 means entering one complete and uniform system. In practice, Medicare is more like a platform with important choices built into it.

Medicare Advantage is where the public and private sides of the system overlap most clearly. It is still Medicare, so it belongs on the government-sponsored side of the map, but the benefits are delivered through private health plans approved by Medicare. Medicare.gov explains that these bundled plans include Part A, Part B, and usually Part D, and that members may need to use network providers or get approval for certain services or drugs. That is why Medicare Advantage often feels more like commercial managed care, even though the program itself is still part of Medicare.

Another important category here is people who qualify for both Medicare and Medicaid. Medicare refers to these individuals as dually eligible. Medicare generally pays first for Medicare-covered services, while Medicaid can help with premiums, cost sharing, and some additional services depending on the person’s situation and state rules. This is one of the clearest examples of how the American system overlaps rather than fitting into perfect boxes.

Commercial coverage for people under 65

For people under 65, the largest commercial category is employer-sponsored insurance. This is the coverage many Americans get through work. The employer usually pays part of the premium and the employee pays part. These plans may be structured as health maintenance organization (HMO), preferred provider organization (PPO), or other network models, but the basic logic is the same: the insurer is private, even if the path to coverage comes through an employer.

The second major category is individual and family coverage sold through the Affordable Care Act (ACA) Marketplace. These plans are sold by commercial insurers but must follow federal rules around consumer protections and essential health benefits. HealthCare.gov explains that Marketplace plans are organized into Bronze, Silver, Gold, and Platinum categories, with Catastrophic plans available in some cases, and that these plans must cover the ten essential health benefit categories, including doctor services, hospital care, prescription drugs, pregnancy and childbirth, mental health care, and more.

People can also buy individual coverage outside the Marketplace. In some cases it still counts as qualifying health coverage, but it does not use the same Marketplace enrollment and subsidy path. That distinction matters because “commercial” does not always mean the government plays no role. Sometimes the insurer is private while affordability is still shaped by public policy.

There are also temporary or narrower commercial pathways. COBRA allows people who lose job-based coverage to continue that same plan for a limited time, usually by paying the full premium themselves. Short-term, limited-duration insurance is another option, but CMS has made clear that it is not the same as comprehensive major medical coverage under the Affordable Care Act and does not follow the same consumer protection framework. It is better understood as temporary bridge coverage than as a full replacement for regular health insurance.

A few other under-65 pathways matter as well. Young adults may remain on a parent’s plan until age 26 in many cases. Some colleges offer student health plans, which CMS describes as a type of individual market health insurance coverage offered to students and their dependents. Some smaller employers use Health Reimbursement Arrangements (HRAs), including Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs), to help employees pay for premiums and certain medical expenses instead of offering a traditional group plan.

Commercial coverage for people over 65

Once people move into Medicare age, commercial insurance does not disappear. It changes role. The best known product here is Medicare Supplement Insurance, usually called Medigap. Medicare.gov explains that Medigap works only with Original Medicare and helps pay some of the costs that Original Medicare does not cover. It is sold by private insurers, and in general you must have Part A and Part B to buy it.

That creates one of the most important forks in the road for older adults. One path is Original Medicare plus a Medigap policy and usually a stand-alone prescription drug plan. The other path is Medicare Advantage, where hospital, medical, and usually drug coverage are bundled through a private insurer inside the Medicare program. Both approaches can work, but they organize premiums, provider access, and out of pocket risk in very different ways.

Some older adults also have retiree coverage from a former employer or union. Medicare materials describe retiree coverage as another source of health coverage people may have alongside Medicare. For households that still have access to it, retiree coverage can reduce cost sharing and fill some of the gaps left by Medicare alone.

Then there are supplemental commercial products, including dental, vision, hospital indemnity, critical illness, and disease-specific coverage such as cancer-only policies. These are real insurance products, but they should be understood for what they are. The National Association of Insurance Commissioners (NAIC) states plainly in its consumer guide that cancer insurance is not a substitute for comprehensive coverage, and NAIC materials also describe specified disease coverage as insurance tied to named conditions such as cancer. These products may help in narrow financial situations, but they do not replace major medical insurance.

Long-term care insurance is another distinct commercial category. It is designed to help pay for extended services such as nursing home care, assisted living, or help with daily activities over a longer period of time. NAIC’s long-term care shopper’s guide treats this as a separate insurance line because it covers a different risk than ordinary medical care. That distinction matters because many people wrongly assume their standard health insurance, or Medicare, will absorb long periods of custodial care. In general, that is not how the system works.

Fee for service and value based care

This is where many explanations go off track. Fee for service and value based care are mainly about how providers are paid, not about what kind of insurance card a person has. Someone can be in a public program or a private plan while their doctors and hospitals are being paid under very different arrangements. Insurance type and payment model are related, but they are not the same thing.

In a fee for service system, providers are generally paid for each service they furnish. CMS explains the physician fee schedule as a system in which payment rates are built from the relative resources used to furnish each service, using relative value units and a conversion factor to calculate payment. In simpler terms, a visit has a payment, a lab has a payment, an imaging study has a payment, and a procedure has a payment. It is a model built around units of activity.

In value based care, payment is tied more closely to quality, coordination, and the total outcome or total cost of care. CMS describes its value-based programs as programs that reward providers with incentive payments for the quality of care they give to people with Medicare. That means the system is trying to pay not only for activity, but also for better management, better outcomes, and lower avoidable waste.

Public programs use both approaches. Original Medicare has historically relied heavily on fee for service payment. At the same time, Medicare also uses value-based models through programs such as the Medicare Shared Savings Program. Medicaid and CHIP also show how mixed the picture can be. Medicaid beneficiary data show that nationally 75.1% of Medicaid beneficiaries were enrolled in comprehensive managed care in 2022, and Medicaid and CHIP managed care often use contracted plans that accept a set per member per month, or capitation, payment.

The same is true in commercial insurance. A person can have a PPO from an employer while the primary care group is in a shared-savings arrangement. Another person can have a Marketplace plan where many providers are still billing service by service. The front-end insurance label explains only part of the story. The payment model underneath shapes incentives, care coordination, utilization management, and how the system tries to balance cost and quality.

The simplest way to remember the system

If you want a workable mental map, think in layers. The first layer is primary medical coverage. Under 65, that usually means employer insurance, Marketplace coverage, Medicaid, CHIP, or one of the military or special public programs. Over 65, that usually means Medicare, either through Original Medicare or Medicare Advantage.

The second layer is cost-sharing support or coordination. That includes Medigap, retiree coverage, and Medicaid support for people who are dually eligible for Medicare and Medicaid.

The third layer is supplemental protection. That includes dental, vision, disease-specific plans, hospital indemnity, and long-term care insurance. Those products can matter, but they sit on top of the main medical structure rather than replacing it.

The fourth layer is payment design. That is where fee for service and value based care sit. Those models shape behavior behind the scenes, and they often explain why two people with different insurance cards may still move through care systems that feel surprisingly similar, or why two plans with similar names can lead to very different provider behavior.

The United States did not build one clean health coverage system all at once. It built several systems over time, then connected them where it could. That is why the whole structure feels messy from the outside. But once you sort it by sponsor, age group, and payment model, the logic becomes much easier to see.

Sources

HealthCare.gov pages on Marketplace plan categories, essential health benefits, qualifying coverage, coverage options for college students and young adults, COBRA, and Health Reimbursement Arrangements.

Medicare.gov materials on Parts A, B, C, and D, the 2026 Medicare & You handbook, Medigap, and Medicare Advantage.

Medicaid.gov materials on Medicaid, CHIP, the Basic Health Program, Medicaid managed care, and CHIP managed care.

Centers for Medicare & Medicaid Services (CMS) materials on the Physician Fee Schedule and value-based programs.

TRICARE, Veterans Affairs, and Indian Health Service eligibility and program materials.

National Association of Insurance Commissioners (NAIC) consumer materials on Medigap, cancer insurance, specified disease coverage, and long-term care insurance.

{kind=link}